LNG Exports for U.S. Jobs, Economic Growth, Trade

Mark Green

Posted January 25, 2013

This week API, on behalf of the U.S. oil and natural gas industry, furnished comments on the Energy Department’s 2012 study of the impact of exporting U.S. liquefied natural gas (LNG). You can read them in full here, but let’s cover some of the main points:

The U.S. has ample natural gas reserves …

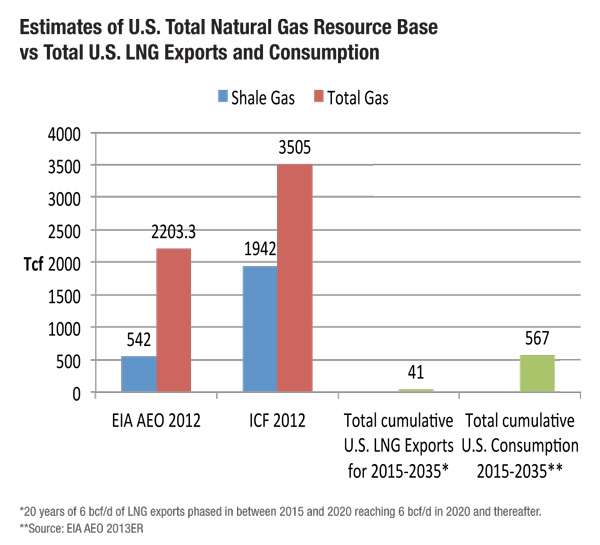

We are the world’s leading producer of natural gas and a global leader in overall natural gas resources, with technically recoverable shale natural gas and total recoverable U.S. natural gas estimated by:

- U.S. Energy Information Administration (EIA) – 542 trillion cubic feet (Tcf) shale; 2,203.3 Tcf overall.

- ICF International – 1,942 Tcf shale; 3,505 Tcf overall.

- Potential Gas Committee – 687 Tcf shale; 1,898 Tcf overall.

.. that will amply support domestic and export markets

U.S. annual natural gas consumption is in the 24 Tcf range, with total cumulative consumption (2015-2035) estimated to be 567 Tcf by EIA. EIA also estimates that 20 years of exports phased in between 2015 and 2020 would generate total cumulative exports of 41 Tcf. Here’s the chart:

API:

“This means that total cumulative exports would consume only 1-2 percent of the total resource base estimated by the ICF and the EIA, demonstrating even greater potential for the U.S. to export LNG.”

LNG exports will stimulate domestic production, job and economic growth …

The DOE study conducted by NERA Economic Consulting found that domestic natural gas production will increase to support exports, creating jobs and boosting direct and associated economic sectors in the process. API:

"LNG exports will create jobs in the oil and natural gas sector, as well as the industries supplying the oil and natural gas sector with materials, equipment and labor. Most studies concur that natural gas production will increase to support export volumes. The NERA study finds that in all three baseline scenarios, natural gas production increases. The EIA has estimated that 60 to 70 percent of LNG exports will be from increased production, with about 75 percent of the increased production coming from shale gas.”

… and U.S. manufacturing will be helped, not hindered

To export LNG, liquefaction facilities – costing in the billions of dollars – will be needed. This will stimulate demand for capital equipment that will cascade through the economy, supporting thousands of U.S. jobs. API:

“Such investment will also lead to a significant increase in permanent U.S. jobs as LNG exports support a higher level of domestic natural gas production, lead to higher supplier industry activity and through the operation and maintenance of the LNG and associated facilities. More specifically, it is estimated that 6 bcf/d of LNG exports would increase U.S. natural gas production by up to 4.2 bcf/d and support approximately 105,000 jobs associated with unconventional natural gas production – not factoring in investment impacts associated with the LNG facilities.”

In addition, increased output of natural gas liquids (NGLs) from overall natural gas development also will provide economic stimulus in the form of NGLs including ethane, which is a primary feedstock for ethylene that’s used to produce a number of different products.

The time is now!

Though the United States is the world’s leading producer of natural gas with ample resources to handle domestic demand and to supply export markets – creating U.S. jobs, stimulating the economy and helping our trade balance – federal officials must approve U.S. export projects without delay or risk seeing international competitors (some of whom have projects under way) win the race to supply those export markets. API:

“… there is a limited amount of global demand for LNG. According to ICF International, the current world LNG liquefaction capacity is estimated to be approximately 37 Bcfd (billion cubic feet/day). A survey of under construction, planned and proposed facilities around the world indicates approximately 49.6 Bcfd of new liquefaction capacity could come online by 2025 outside of the U.S. Add to that the fact that approximately 28.7 Bcfd of U.S. liquefaction capacity could come online if all FTA applications in the U.S. Department of Energy Docket as of Nov. 21, 2012 become operational. The expected worldwide demand for LNG falls far short of potential 115 Bcfd of world LNG supply. Various projections show that expected world demand for LNG will be in the range of approximately 50 Bcfd to 65 Bcfd by the year 2025. This clearly indicates that a significant share of the proposed liquefaction capacity will not be built.”

Shorter: Not all export projects around the globe will be built, because world demand won’t support them all.

So the question: Will these LNG export projects be built in the United States, or will potential U.S. projects be shelved because competing facilities elsewhere were built first? That’s what the LNG debate really comes down to. A number of studies, including this one from Brookings, have said exports’ impact on domestic natural gas prices will be modest – while the overall lift to our economy will be significant – so that’s not the key issue. The real point is whether America’s vast natural gas resources will be put to work for Americans, creating jobs and projecting growth throughout the economy.

About The Author

Mark Green joined API after a career in newspaper journalism, including 16 years as national editorial writer for The Oklahoman in the paper’s Washington bureau. Previously, Mark was a reporter, copy editor and sports editor at an assortment of newspapers. He earned his journalism degree from the University of Oklahoma and master’s in journalism and public affairs from American University. He and his wife Pamela have two grown children and six grandchildren.