Natural Gas Abundance Generates Export Opportunities

Dean Foreman

Posted February 28, 2018

In the first API Chart of the Month, we looked at historical U.S. trade in oil and natural gas. This month, let’s examine global liquefied natural gas (LNG) prices, which increasingly have helped to anchor U.S. natural gas production and reinvigorate local jobs, wages, housing, education and services – everything that comes with major new capital projects and their broad-based boost to the economy.

Highlights:

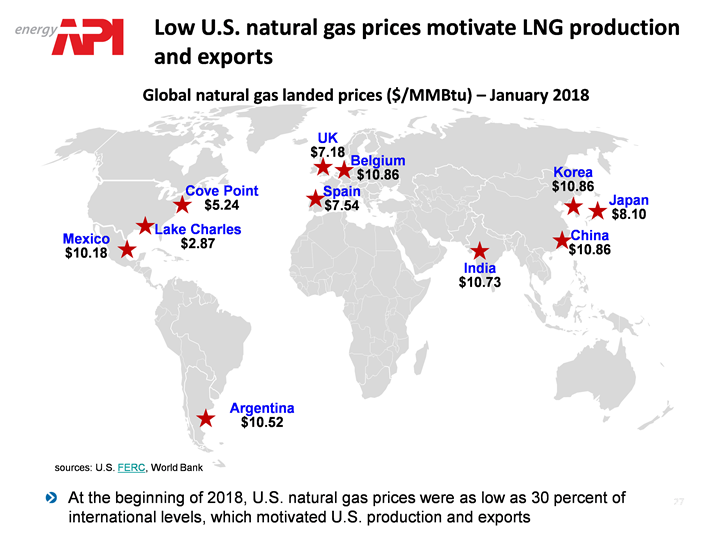

- Spot LNG prices in January exceeded $10 per million Btu (MMBtu) in many countries and typically are priced in relation to crude oil via long-term contracts that are specific in volume and destination, which prevents reselling cargos.

- Importantly, domestic U.S. natural gas prices have remained low even as U.S. exports of LNG quadrupled in 2017 to nearly 2 billion cubic feet per day. The U.S. Energy Information Administration expects natural gas prices at Henry Hub to remain below $3 per million btu in 2018.

- The roughly $8/MMBtu difference between domestic U.S. and international LNG prices provides an incentive to export even more LNG from the U.S., which in turn means greater U.S. investment, exports and economic opportunity are possible as natural gas markets continue to grow and globalize.

- U.S. LNG import prices, unlike those in other regions, generally are priced via short-term contacts and include a reference to domestic natural gas prices. U.S. LNG import prices therefore are outliers globally due to the abundance and low cost of U.S. natural gas.

- Why does the U.S. still import LNG? Once hundreds of millions of dollars are invested in building an onshore terminal to import, store and re-gasify LNG, there’s a strong economic incentive if not a contractual obligation to utilize the facilities. Many U.S. import terminals have converted to export terminals, and this trend may continue.

As the U.S. energy renaissance matures, it’s easy to forget how it felt 10 years ago when domestic natural gas prices were upwards of $13/MMBtu. Natural gas prices and price volatility have been relatively low ever since then – largely thanks to abundant domestic production from shale and other tight-rock formations.

And as U.S. consumers and manufacturers have continued to enjoy an extended era of low prices, U.S. communities have experienced growth that manifests in terms of gains in employment, wages and a reinvigoration of local housing, education and services – everything that comes with building major new capital projects and having solid employers help anchor the economy.

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.