Unintended Consequences in Alberta's Limits on Crude Output

Dean Foreman

Posted February 19, 2019

A profound shift has taken place in North American oil markets over the past few months that’s now affecting trade between the United States and its biggest crude oil supplier, Canada.

It involves supplies of heavier crude oil – important for the manufacture of a multitude of everyday products consumers use, from local road surfaces to the roofing for their houses. While the U.S. is producing domestic crude at record levels, there’s still a need for heavier crudes.

With heavy oil from Venezuela declining for years, the importance of close ties with Canada and especially the oil-producing province Alberta has increased. Unfortunately, Alberta’s decision to limit oil production appears to be advancing uneconomic outcomes, where some U.S. refiners signaled they’ll shift away from Canadian heavy crude oil and seek supply elsewhere.

As with any market intervention, there are likely to be unintended consequences. Canada should be cautious if it incentivizes its largest buyers to shift away from Canadian oil.

Details follow, but first some background.

In this post, Why the U.S. Must Import and Export Oil, we explained the importance of crude oil quality, quantity and geographic location in meeting the needs of American industry and consumers.

One important quality dimension is whether oil is light or heavy, and heavy crude oil such as that from Venezuela or Canada has expanded our oil resource and supply potential as well as the varieties of molecules that are needed to make essential everyday products, including chemicals, lubricants, waxes and materials for roads and roofs.

Consequently, many U.S. refiners have configured their facilities to be able to process heavy crude oil and in doing so made substantial capital investments in additional refining processes, such as cracking or coking, or so-called conversion capacity.

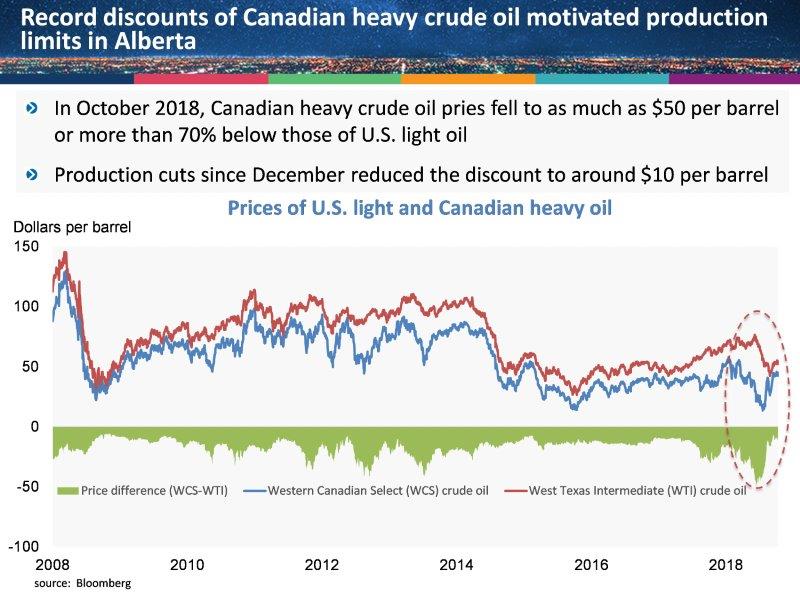

With the requisite additional investment and processing costs, heavy oil typically has been priced less than light oil. Since 2008, the Western Canadian Select (WCS) heavy oil traded at an average discount of $17.25 below West Texas Intermediate (WTI) crude oil, according to data from Bloomberg. And, with the decline in Venezuelan production, the U.S. has turned to Canada for greater heavy crude supply.

Notably, Canadian producers stepped up and increased production faster than the market’s capacity to transport or store the oil could grow, so Canadian heavy oil prices decreased. In October 2018, when WTI crude oil averaged $71 per barrel, WCS crude oil fell to $21 per barrel – a record discount of $50 per barrel or 70 percent. We know that markets work, however, and at such relatively low prices U.S. refiners sought as much Canadian oil as possible, importing a record 4.2 million barrels per day (mb/d) in November, per the U.S. Energy Information Administration.

Rather than riding out the price downturn and empowering the pipeline and rail transportation sectors to respond to the record demand for their services, the Alberta government late last year asserted that low prices were “costing the national economy $80 million per day.” Consequently, Alberta intervened in the marketplace and forced Canadian companies to cut 325,000 barrels per day (kb/d) of oil production until 35 million barrels of oil currently in storage is shipped to market.

Now let’s fast-forward to mid-February, when the discount of WCS crude oil fell to less than $10 per barrel below WTI. Compared with the past decade, this was an exceptionally narrow difference between WCS and WTI prices – among the top decile since 2008. However, rather than discontinue or relax the production restraint at these relatively strong WCS prices, Alberta has continued to intervene in the market and distort prices via the mandated production cuts.

However, some major producers have recently indicated WCS prices have risen too high in relation to alternatives, so they see it as no longer economic to ship Canadian oil to the U.S. via rail. In fact, Bloomberg data show mineral shipments on the Canadian Pacific railway over the past four weeks (as of early February) were down 22 percent compared with one year ago. The province could therefore be selling less oil and missing out on infrastructure investments to position for future growth.

For example, in an excellent recent podcast by Arc Energy Institute, Canadian National Railway explains how the large investments in new rail cars, locomotives and infrastructure needed to expand shipping of Canadian oil to the U.S. have evolved from a daily transactional business into one that necessitates longer-term planning with three-year commitments as well as shortfall penalties. It would be difficult just now to take a long view on the enabling infrastructure when the government’s market interventions have undermined the economics of utilizing WCS.

Alberta’s slogan is to “be part of the energy.” Market interventions like Alberta’s ultimately are a lose-lose proposition for all stakeholders, despite having boosted WCS prices in the very short term, and one of the few pathways by which they could seriously impede markets for Canadian heavy oil.

As API has consistently emphasized, sustaining the energy revolution and the economic benefits it can offer requires cogent energy policies, infrastructure and free trade. To “be an integral part of the energy,” Alberta’s long-term prize could be to foster a robust and enduring crude oil supply relationship that plays a role in helping to maximize the competitiveness and efficiency of the entire North American energy system, from resource development all the way to ultimate manufacturing performance.

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.