U.S. Global Oil Leadership to Continue – Which is Great for Economy

Dean Foreman

Posted February 26, 2019

In case you missed it, let’s echo a recent official U.S. Energy Department projection that the United States should “not only maintain its lead spot as top oil producer, but will greatly exceed what it produced last year in both 2019 and 2020.”

The trajectory of U.S. oil production is significant for U.S. economic growth, energy security and global leadership, and – as we recently discussed oil exports in this post – potentially raises the stakes in the market share battle between the United States and OPEC plus Russia (OPEC+).

Specifically, in API’s latest Monthly Statistical Report (MSR), we highlighted record U.S. production of crude oil (11.9 million barrels per day (mb/d) and natural gas liquids, 4.9 mb/d). In its latest Short-Term Energy Outlook, the U.S. Energy Information Administration (EIA) projects oil production to grow to 12.4 mb/d in 2019 and 13.2 mb/d in 2020. EIA says natural gas liquids (NGL) production will reach 5.5 mb/d in 2019 and 5.9 mb/d in 2020, and natural gas production will total 90.2 billion cubic feet per day (bcf/d) in 2019 and 92.1 bcf/d in 2020.

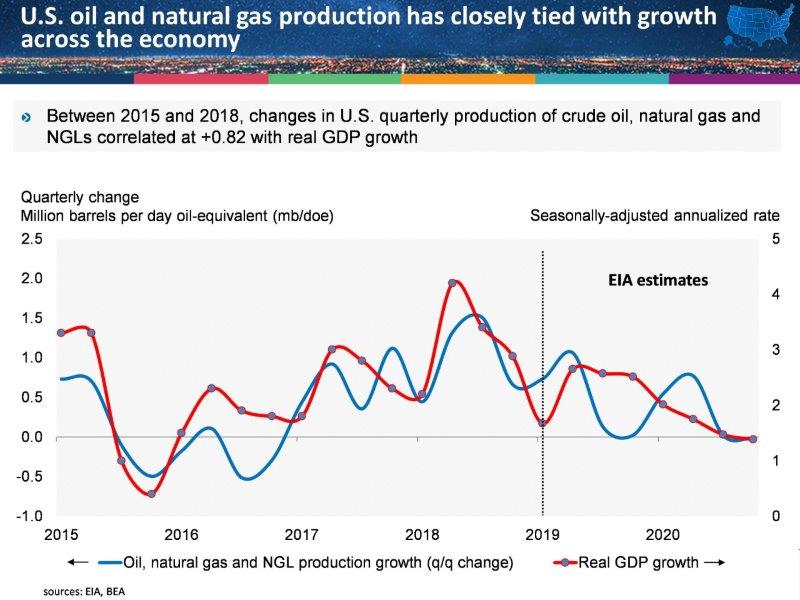

That’s a lot of numbers, but they’re meaningful ones. Perhaps no other sector is as closely tied to the overall economy’s performance – as measured by real GDP growth – as natural gas and oil.

Since 2015, the simple correlation is +0.82 between the quarterly changes in total crude oil, natural gas and NGL production and real GDP growth, as the chart below highlights:

EIA projects a slowing of U.S. energy production and economic growth over the next two years, which underscores the importance the energy revolution.

It’s not a spurious correlation given the hundreds of billions of dollars in industry investment throughout the economy to leverage these new-found energy sources, including resource development and production, pipelines and processing, refinery and petrochemical expansions, export facilities, natural gas-fired power plants and energy-intensive manufacturing.

There also are benefits to American consumers through lower energy prices, as well as key inputs associated with many manufactured goods. With this perspective, it’s easy to see why the U.S. energy revolution has been historic in its impacts and arguably the best thing that has happened to the U.S. economy since the Internet boom in the late 1990s.

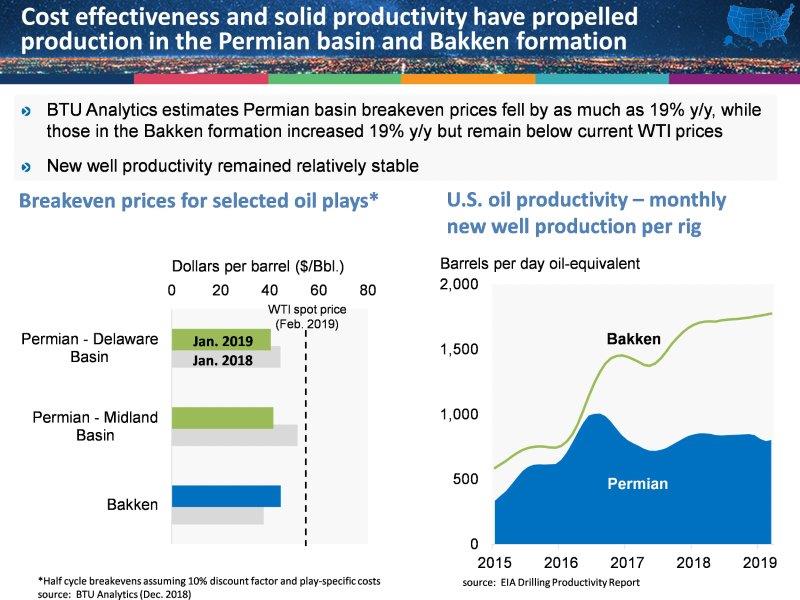

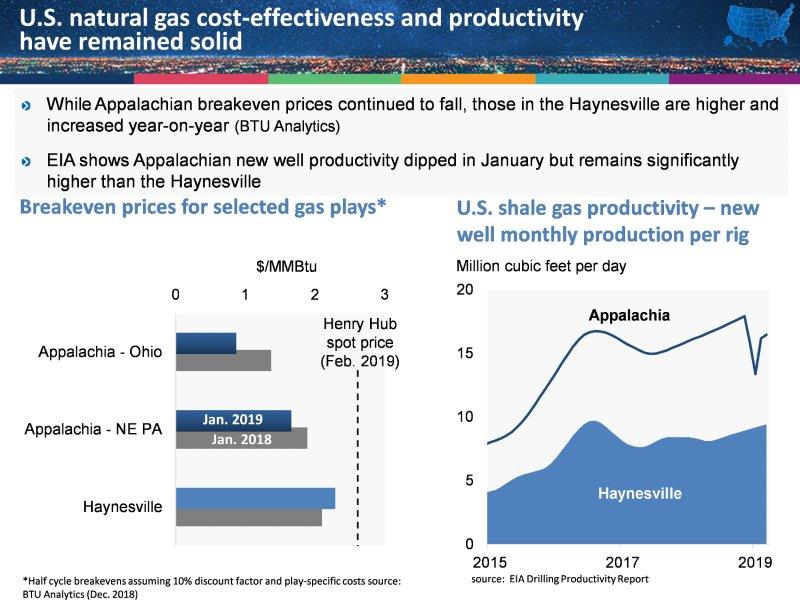

Given the large recent declines in oil and natural gas prices, it’s logical to ask next about the health of the industry. In terms of the prices needed to break even on drilling oil or natural gas wells as estimated by BTU Analytics, the next two charts show for oil and natural gas, respectively, that current prices should on average be sufficient to underpin production growth within the major shale plays. Moreover, EIA’s estimates of oil and natural gas rig productivity in terms of monthly production per rig appear to have sustained relatively strong levels, despite some variability in the Appalachian region in January.

These figures comprise trends that should support the EIA’s projections for U.S. production growth to 2020. Additionally, the backlog of drilled but uncompleted wells neared a record 8,900 wells in January per EIA, so production could come even if drilling were to slow.

If we accept EIA’s projections with conviction and juxtapose them with the agency’s estimates of U.S. natural gas and oil demand growth, it’s amply clear that the expansion of U.S. infrastructure and exports to global markets are associated with strong economic and energy growth and security. More to come on that in API’s next Industry Outlook due on March 14. Watch this space!

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.