Electric Vehicles: If You Build Them, Will Buyers Come?

Dean Foreman

Posted March 11, 2020

Several states are taking the lead to promote electric vehicles (EVs), and they’re not the states that produce them. From California and Oregon to New Jersey and Maryland, their promotions are mainly efforts intended to reduce carbon dioxide emissions.

But even with large state incentives, are consumers onboard?

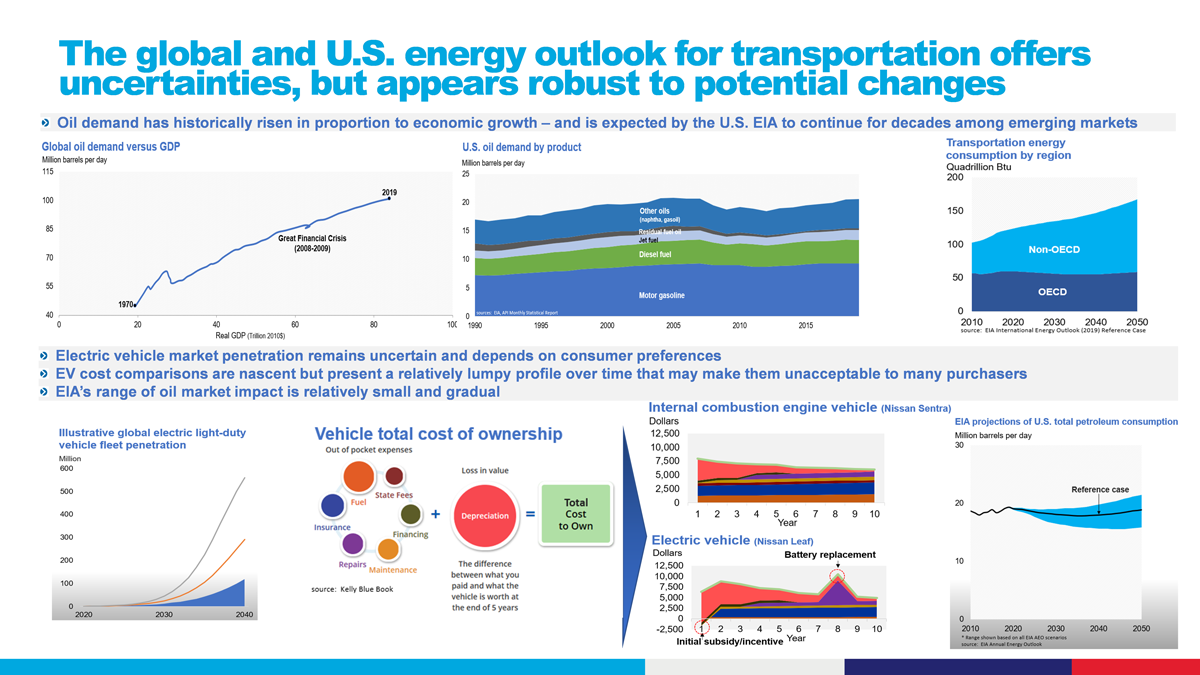

It’s an important question because it’s unclear whether Americans will embrace EVs on a scale needed to reduce emissions as much as proponents say they will.

Demand usually dictates product development, not the other way around. In light of recent data on vehicle total cost of ownership, it’s fair to ask whether a critical mass of consumers can be coaxed into buying these vehicles.

Automotive manufacturers are positioned to introduce around 500 new EV models through 2023, per McKinsey. So, the next few years should test the hypothesis of “If you build it, they will come.” That may apply to building a baseball diamond in the middle of an Iowa cornfield, but it’s unclear whether policy can motivate technology that ultimately drives consumer purchases.

Currently, consumer preferences appear to be a material uncertainty for EVs. No one knows what underlying demand for EVs could look like in the next few years – especially when consumers reckon the cost of owning and driving one.

When we look at total cost of ownership (TCO) data from Edmunds side-by-side for comparable electric and gasoline- and diesel-fueled vehicles, such as Nissan’s Leaf EV and its Sentra, some interesting facts arise that offer clues about the potential for EV growth in the marketplace.

Importantly, depreciation remains the largest portion of vehicle ownership cost, and at least some EVs have depreciated above and beyond the higher amount one would expect given that an EV today is much more expensive than a comparable conventional vehicle. Just as consumers’ valuation of a 5-year old iPhone is limited, EVs also may be viewed like a consumer electronic. A weak secondary market would seem to be a characteristic that is unlikely to change as the wave of new models comes over the next few years.

Another and perhaps less-apparent point of the side-by-side TCO comparison is that the cost of a conventional vehicle is relatively smooth over time, while the cost for an EV depends on up-front monetary incentives as well as eventual battery replacement costs.

Take the Nissan Leaf, where battery replacement reportedly costs between $5,500 and $8,500 after seven to 10 years. The prospect of spending that kind of money to replace the battery could put the Leaf out of reach for the 50% of U.S. households earning less than about $63,000 per year – even if the vehicle is purchased inexpensively in the secondary market.

Economics contribute to consumer preferences, which also may depend on utility, performance, aesthetics and brand preference among other factors. However, if the basic economics of a vehicle do not make sense from a consumer’s perspective, the prospects for repeat purchases could be weak, and then it becomes a gamble for manufacturers as to whether their next generation of EVs – again, compared to conventional vehicles – evolves enough to enable the purchasing cycle to repeat, and on what scale.

In the aggregate, the societal costs of EVs – if scaled to support light-duty vehicle fleets with low- or zero-emitting sources – including needed generation, transmission, distribution and charging infrastructure for homes and commercial locations, looks like a relatively costly way to address emissions.

While we talk about the potential for EVs to disrupt petroleum markets, we also must consider so-called opportunity costs. U.S. productivity in oil and natural gas production has, per the U.S. Energy Information Administration (EIA), demonstrably benefitted from innovative technologies – 3D imaging, horizontal drilling, hydraulic fracturing and analytics that enable real-time learning – that together set a high bar economically for alternatives to overcome.

Although lower near-term petroleum demand is anticipated with global measures to stem transmission of the coronavirus (COVID-19), oil and natural gas prices at historically low levels have tended to stimulate demand along with the economy, globally and in the United States. Remarkably, U.S. oil demand in 2019 was at its highest level since 2007, according to API estimates.

Looking forward, recent endorsements of the U.S.-China Trade phase one agreement and U.S.-Mexico-Canada Agreement should reinforce economic and energy growth, domestically and internationally. On top of that is consensus at the World Economic Forum in January, anticipating that global growth will stabilize this year, which should also advance global oil demand as well as the prospects for an energy transition.

The bottom line is that forecasts by EIA and other governmental sources for long-run petroleum demand suggest that while EVs will grow in the marketplace, that growth will be within a relatively narrow band characterized by gradual changes. This conforms with recent history, to the benefit of drivers everywhere.

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.