Here’s Why U.S. Natural Gas Has Weathered the Pandemic

Dean Foreman

Posted July 21, 2020

Through the recent COVID-19 pandemic and resulting shocks to energy markets around the world, U.S. natural gas has remained a relatively bright spot.

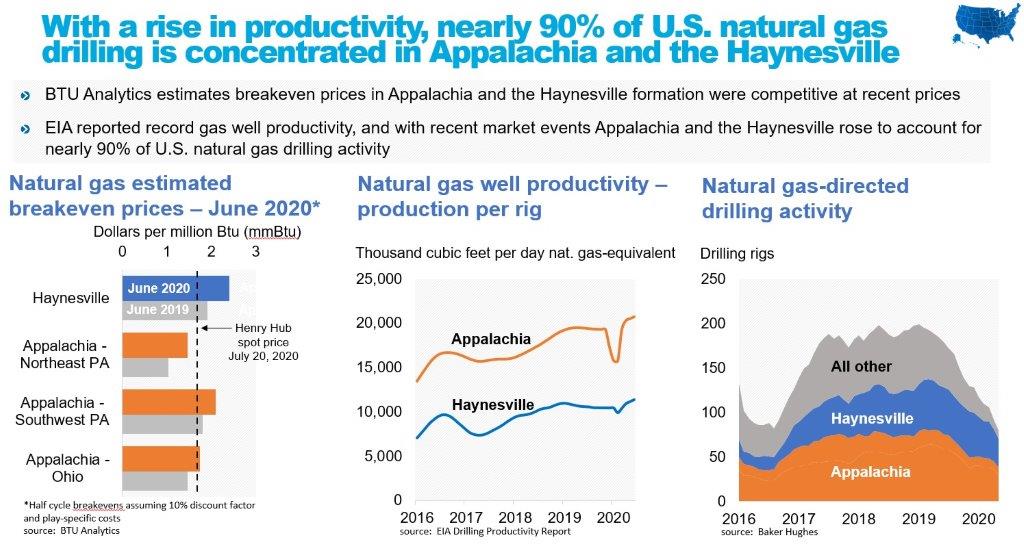

Record low prices have benefitted consumers, and at the same time many producers dedicated to natural gas in Pennsylvania, Ohio, West Virginia, Louisiana and East Texas have remained viable as cutbacks in oil and associated natural gas from other regions have taken effect. And now about 90% of U.S. drilling for natural gas is concentrated in these regions, that is Appalachia and the Haynesville areas.

The drilling activity has reflected two fundamental observations. The first is that, according to BTU Analytics, the recent breakeven price – that is, the Henry Hub wholesale market price needed to at least break even in drilling a new well – on average has remained near market prices despite COVID-19, a relatively warm winter and broad financial market concerns.

The second observation is that natural gas well productivity, as reported by the U.S. Energy Information Administration, were resilient after some unexplained variation at the beginning of the year. EIA’s estimates partly reflect actual past production trends, so this is a sign that the results being achieved on the ground have remained positive.

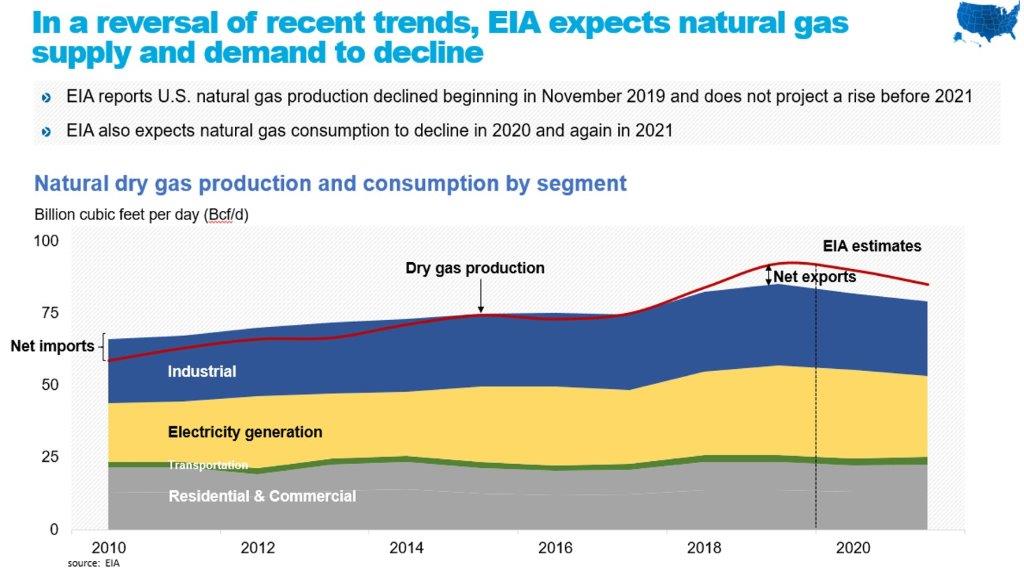

Next, let’s turn to U.S. natural gas demand, also by EIA estimates.

In recent years, U.S. natural gas demand has expanded rapidly, especially in electricity generation and exports of liquefied natural gas. However, a shift that EIA currently projects is that this growth may subside along with the recent slowing of economic growth. If this plays out as EIA expects, it’s an important potential signal for U.S. natural gas production, as by economic fundamentals supply generally lags demand in responding to market conditions.

The potential for the production trend to turn suggests that natural gas producers have responded rationally and are attempting to grow their businesses based on their existing cash flows. But this should not be interpreted as a sign of weakness.

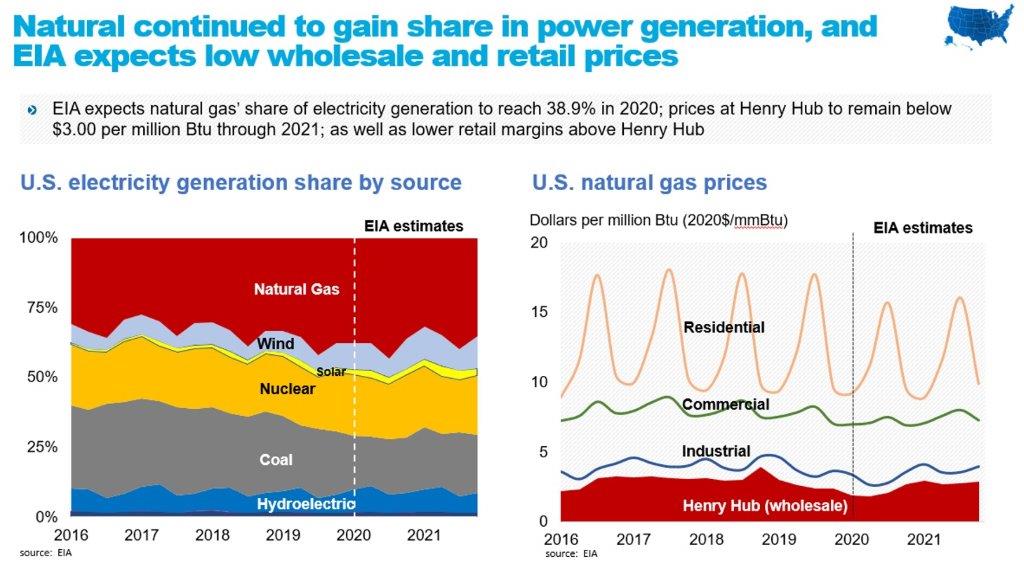

Rather, U.S. natural gas production has never been more cost-competitive than it is today. To see this, notice the record 38.9% market share that natural gas won within electricity generation at the end of 2019.

The market share has also corresponded with broadly lower wholesale and retail natural gas prices, which have fallen across all sectors in recent years and better enables U.S. businesses and households to benefit from lower costs.

In this sense, the sweet spot where consumers and producers can both be advantaged shows how the U.S. energy revolution has continued to evolve through even as the macroeconomic backdrop and broader business cycle have continued to change.

In this sense, these data show a source of resilience that was largely unexpected even by those in the industry as recently as last year. And it shows how dedicated natural gas drilling has remained a viable business in the U.S. throughout it all.

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.