The Ups, Downs and Ups of 2020 Show Resilience of U.S. LNG Exports

Dustin Meyer

Posted February 5, 2021

We learned some important things about U.S.-exported liquefied natural gas (LNG) in the whiplashing of natural gas markets last year – from record highs at the start of the year to an unexpected drop by midyear and then back to record highs in 2020’s final months as demand came roaring back.

First, the extreme ups, downs and ups of 2020 underscored two of the characteristic strengths of the U.S. LNG export industry – its flexibility to changes in demand and its resiliency in the face of immense market challenges.

Second, the rapid rebound of U.S. LNG exports from deep troughs in the middle of the year emphatically answered questions raised by some about the long-term viability of natural gas demand.

Third, forecasts that the business case for U.S. LNG exports were permanently harmed, as price indices converged last year, now seem premature.

And fourth, the sharp decrease in demand from the pandemic looks like an outlier, not the new normal. If anything, the main trend driving the resurgence of U.S. LNG exports – robust and growing LNG demand in Asia – appears set to continue, according to the International Energy Agency (IEA).

Surging Demand Pulls U.S. LNG out of Historic Slump

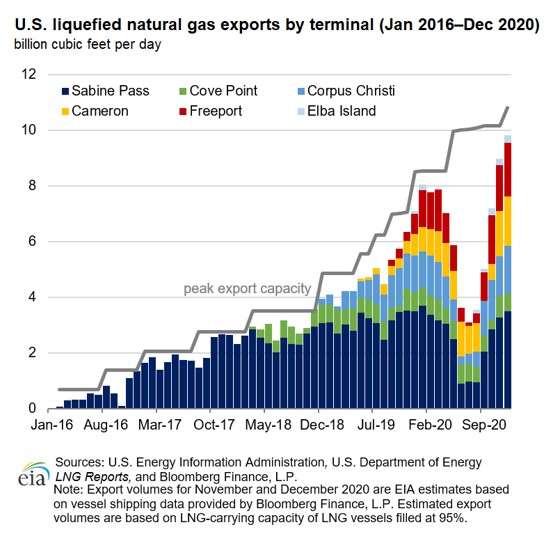

U.S. LNG exports started 2020 off strong. After a record-breaking year in 2019, LNG exports hit at what that time was a record 8 billion cubic feet per day (Bcf/d) in January. LNG exports remained strong through March, but in April the COVID-related drop in demand began to show up as a decline in exports.

The period from April to July saw back-to-back, month-on-month decreases in exports. By the time July rolled around, average exports dropped to a level (3.1 Bcf/d) not seen since May 2018, when the available liquefaction capacity in the U.S. was around one-third the current capacity. During one week in July, weekly exports reached a nadir not seen since December 2016, when there was only one LNG export facility with two trains in operation (there are now six LNG export facilities in the U.S. with a total of 15 standard-size LNG trains and 10 small-scale Moveable Modular Liquefaction System units).

Export volumes started to pick back up last August, but disruptions from an historically active storm season in the Atlantic dampened the recovery. It wasn’t until Q4 2020 that exports really started to take off. Both November and December saw record-breaking exports on a monthly average basis, reaching 9.4 Bcf/d and 9.8 Bcf/d, respectively, the latter being more than 20% above the previous record set in January 2020.

The story of record-high LNG exports bookending 2020 is noteworthy enough. Even though the record-high spot prices seen in Asia last month have moderated, they are still elevated from what was seen prior to the 2020 price crash. This shows that market growth is being driven by increasing demand, especially in the heating and power sectors in Asia, while fulfilling the need for a reliable and price-competitive source of natural gas in the global market.

However, U.S. LNG exporters’ strong performance in Q1 and Q4 2020 is all the more noteworthy given the difficulties the industry faced in the middle-half of the year, when demand sharply declined as the COVID pandemic peaked. As a result of that decline, global natural gas markets experienced their largest recorded drop in consumption – an estimated 2.5% year-on-year decrease (approximately 3530 billion cubic feet, or 100 billion cubic meters). And yet, despite this record drop in consumption, global LNG trade still expanded 2%, according to the IEA‘s Gas Market Report for Q1 2021.

What does this resurgence mean for U.S. LNG exports in 2021?

Again, if anything, LNG exports’ up-and-down ride over 2020 shows the resilience of the U.S. LNG industry amid unprecedented conditions driving down demand during the spring and summer. Estimates are that as many as 200 cargoes were canceled last summer. Export volumes reached levels not seen since the U.S. had one-third of its current export capacity, and yet, the U.S. LNG industry was able to adapt – both when demand plummeted and now that it is surging again.

Difficult periods such as 2020 show how important the U.S. LNG industry is as a swing supplier to the global market. In the short-term, the rebound in natural gas prices from increased demand could help push final investment decisions for new U.S. liquefaction terminals over the goal line in 2021.

While the spike in prices in the latter part of 2020 and the early weeks of this year was weather-driven (specifically, it was a severe cold snap in Northeast Asia), it also highlights an important dynamic underlying long-term LNG demand. What is this dynamic? Fast-growing, developing countries in Asia that see natural gas as an integral and growing part of their energy mix, and not just in the power sector.

Case in point, one factor that likely contributed to the run-up in prices was the new demand created by the millions of households in China that switched from coal to natural gas for heating their homes last year. Several months prior to the price spike, China’s Ministry of Ecology and Environment proposed transitioning more than 7 million households in the country’s north off coal by October 2020. The last time Chinese cities saw a wave of largescale coal-to-gas switching in residential heating over the 2017-2018 winter, it triggered a similar spike in LNG prices, pushing them up to $25 per million British thermal units. It is no surprise then that out of the three Northeast Asian countries that imported the most LNG last December, China imported the largest volume.

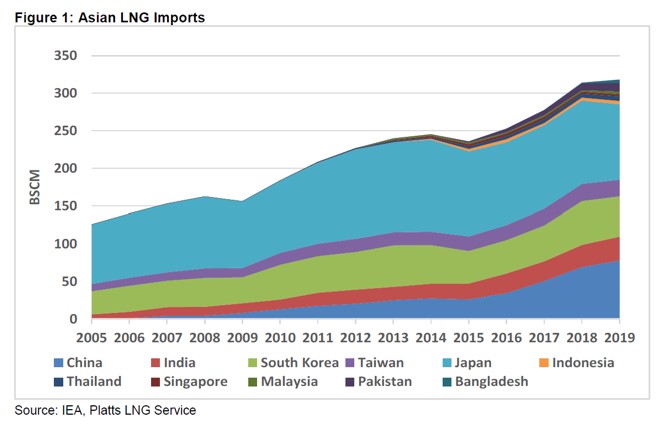

Now that prices have moderated, the markets are showing a return to the long-term trend of increasing demand for natural gas in Asia, as seen in the figure below from the Oxford Institute for Energy Studies report on emerging Asia LNG demand. Though the figure only goes out to 2019, the trend of steadily growing LNG demand prior to COVID-19 is evident. When taking into account IEA’s estimation that Asian natural gas demand is projected to rebound strongly in most key growth markets in 2021, it does appear that last year’s demand plunge from the COVID-19 pandemic was more of an interruption to a long-term trend than a paradigm shift in gas market dynamics.

We see further evidence of this long-term trend in the stated energy policies of some of these key Asian growth markets. Take India, for example. As part of its goal to increase the share of natural gas in its primary energy mix, from the current 6% to 15% by 2030, India’s Minister of Petroleum and Natural Gas Dharmendra Pradhan said Dec. 2 that the country would see $66 billion of investment in natural gas infrastructure.

In China, the formation of PipeChina in early 2020 – and the increased access to the natural gas distribution network it has afforded – is expected to spur a bevy of investments in LNG import capacity by city gas distributors and companies other than China’s three major national oil companies. By 2030, these buyers are expected to quadruple their LNG receiving capacity, eventually accounting for 40% of China’s overall capacity and helping to propel China toward being the top LNG importer in the world by 2022.

Both of these developments are in line with IEA projections that markets in emerging Asia, led by China and India, will drive global demand growth for LNG imports out to at least 2025.

Altogether, projections such as these paint a picture of an industry that will continue to grow after rapidly recovering in the last couple of months of 2020. Like other industries, the U.S. LNG industry took a hit from the COVID-19 pandemic, but its flexibility, reliability and resiliency in responding to swings in global demand will only help make it an even more important LNG supplier in the coming decades.

About The Author

Dustin Meyer is Senior Vice President of Policy, Economics and Regulatory Affairs, leading API’s public policy departments and overseeing the organization’s economics, research, and regulatory functions.

He previously served as API’s Vice President of Natural Gas Markets, dealing with issues related to domestic and global natural gas markets, as well as natural gas technology and innovation including renewable natural gas, differentiated/responsibly sourced natural gas, hydrogen and the use of CCUS in the power sector.

Prior to joining API, Meyer led analytics, forecasting and consulting services on global LNG and renewable energy markets for Energy Ventures Analysis. He also held analysis positions at PFC Energy and then IHS Energy on upstream investment in North American oil and natural gas, including liquefaction projects in the U.S. and Canada. Meyer also worked at ICF International on the transportation policy team and for various NGOs.

He earned his undergraduate degree at Princeton University and received his Master’s focused on Energy Policy & Economics from Yale University.