More on Variations in State Gasoline Prices

Dean Foreman

Posted July 6, 2018

Earlier this week we looked at the summer variation in gasoline prices, due mainly to increased driving as well as fuel specifications that have added to the cost of gasoline. As the 2018 summer driving season approaches its midpoint, let’s check the data on gasoline prices and, separately, take a deeper look at why prices in any one state have tended to be higher (or lower) than the national average.

According to the American Automobile Association, the nationwide average price for regular gasoline was $2.85 per gallon on June 28, a decrease of 12 cents per gallon since May 28.

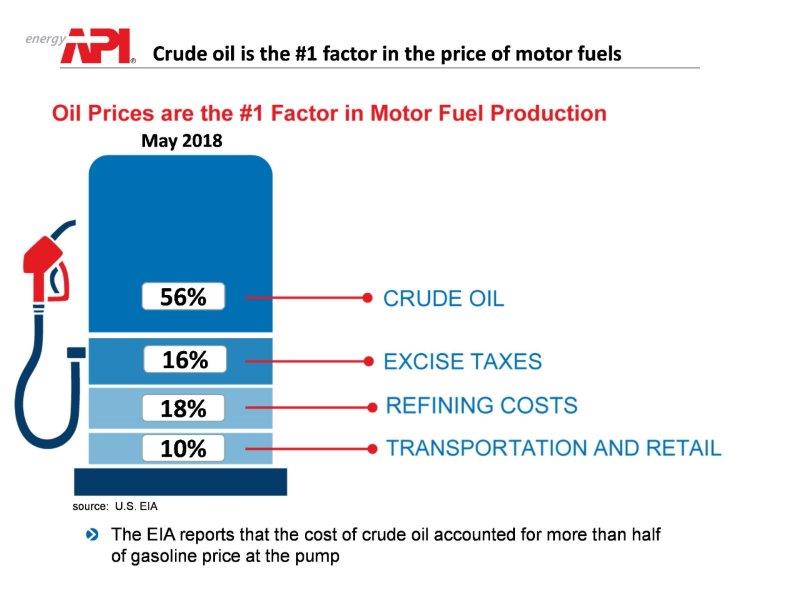

Remember, gasoline and diesel fuel prices tend to track the price of crude oil, because crude oil currently makes up more than half of the cost to make the fuels. The U.S. Energy Information Administration (EIA) reported that crude oil made up 56 percent of the price of gasoline in May, the agency’s most recent analysis.

In June, data from Bloomberg showed that monthly average West Texas Intermediate (WTI) crude oil price fell by $2.50 per barrel from May, which accounted for about half of the 11 cents-per-gallon decrease in gasoline prices. Due to the fixed amounts of state and federal gasoline taxes and fees, seldom does the comparison of monthly percentage changes in gasoline and crude oil prices match so well.

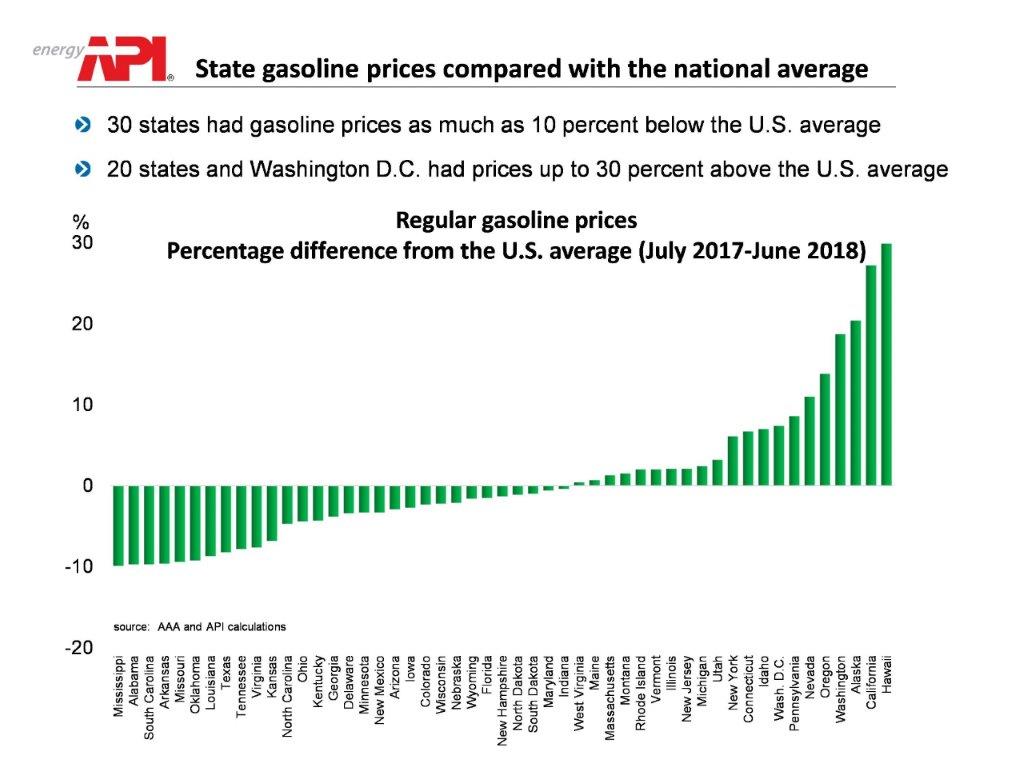

This leads to the question that I’ve received the most: Why are gasoline prices in certain states higher or lower than the national average? Specifically, is it fair to attribute the price differences to state taxes and fees?

To answer this, consider average regular gasoline prices by state over the past year (July 2017 to June 2018). The average for the year of $2.57 per gallon was skewed by a handful of states with relatively high prices, as shown below. Twenty states plus Washington, D.C., had prices as much as 30 percent above the national average, while 30 states had prices that were as much as 10 percent below the national average.

Next, let’s attempt to explain these differences based on the following variables:

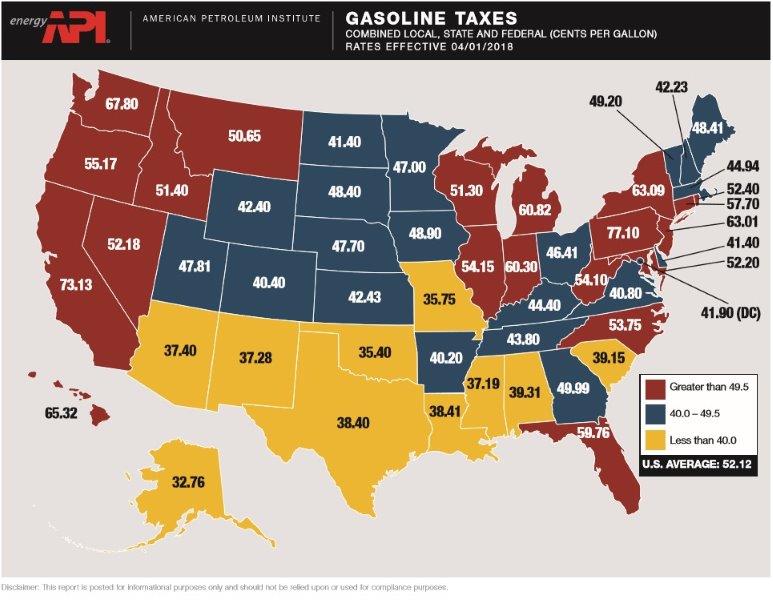

- The amount of state taxes and fees (see below); and,

- State population density, as the most densely populated states tend to be farther from oil production and refineries and may have higher prices from higher transportation costs.

Additionally, let’s consider whether a state brought in gasoline from a relatively low-cost source. Specifically, the EIA reports gasoline flows between Petroleum Administration for Defense Districts (PADDs). States that bring in gasoline from the mid-continent (PADD 2) and U.S. Gulf Coast (PADD 3), where most of the nation’s refining capacity is located, should have relatively lower prices.

Finally, for completeness, we’ll account for discrete differences among states, including whether state regulations require oxygenated fuel in most areas and, separately, whether a state is part of the contiguous U.S. lower 48 states – versus Alaska and Hawaii, where a number of products tend to be more expensive because of the costs to transport items the long distances from production/supply centers in the Lower 48.

Here’s what we found based on a highly significant regression analysis of the historical data:

- State taxes were the most important factor in whether a state’s gasoline prices were above or below the national average.

- States that bring in gasoline from the mid-continent or U.S. Gulf Coast tended to have prices that were significantly lower than the national average.

Therefore, when consumers ask why a given state’s gasoline prices differ from the national average, differences in state taxes and fees are the main reason.

Importantly, however, there also have been consumer benefits to infrastructure that enhances a state’s ability to receive gasoline from low-cost oil production and refining hubs in the mid-continent and U.S. Gulf. This is one reason it can be beneficial for a pipeline to travel through your state. Ultimately, we’re all consumers, and a well-connected market is best positioned to function efficiently and deliver benefits.

As we move forward, policies that foster U.S. natural gas and oil production, support international trade, avoid tariffs that hamper the economy, and foster infrastructure development and investment growth are critical to the energy renaissance.

Enjoy the rest of the summer driving season!

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.