MSR: Record Pull for U.S. Oil Exports in April Spurred Historically Low Inventories

Dean Foreman

Posted May 19, 2022

API’s new Monthly Statistical Report (MSR™), with primary data through April, sheds light on how Americans have been coping with record-higher motor fuel prices amid a genuine global energy crisis:

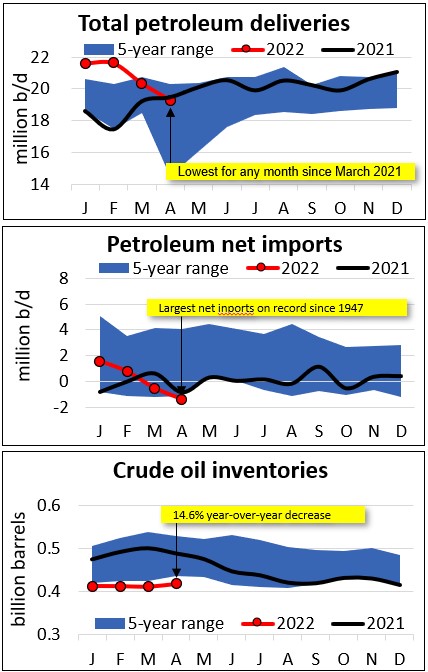

- U.S. petroleum demand (19.3 million barrels per day or mb/d) decreased to its lowest for any month since March 2021.

- With Russia’s war in Ukraine, U.S. petroleum net exports rose to 1.4 mb/d, their highest on record since 1947.

- U.S. crude oil commercial inventories (excluding the Strategic Petroleum Reserve) were the lowest for April since 2014 and showed the lowest year-to-date stock building on record since 2005.

The most frequent question these days is whether the data show evidence of any lower petroleum demand with recent price increases. Although a month or two of data does not constitute a trend, it appears that a combination of slower economic growth, emergence from the pandemic, and historically high prices have impacted U.S. petroleum demand.

Specifically, demand fell by 0.1 mb/d in March and by another 1.0 mb/d in April. Excluding the 2020-2021 pandemic, this was the largest two-month decrease since September 2008.

The vast majority – over 90% – of the fall was in “other oils” – naphtha, gasoil, propane and propylene – that feed refinery and petrochemical operations that make consumer products such as medical plastics, films and packaging. This suggests there was less demand for these products as the economy has emerged from the pandemic.

As motor fuel prices remained near record-high levels, however, U.S. gasoline demand remained flat (compared to seasonal increases historically since 2012), and distillate fuel oil demand dropped for a second straight month, consistent with reports of slowed freight trucking. Jet fuel demand picked up seasonally in April. Notably, residual fuel oil demand tripled year-on-year with fuel substitution and strong marine bunker fuel consumption.

Now for the supply side. U.S. crude oil production rose by 158,000 barrels per day (b/d) in April but was offset by a 130,000 b/d decrease in natural gas liquids (NGL) field production. Meanwhile, U.S. refinery activity remained solid with a capacity utilization rate over 90% for the second straight month.

And with the potential loss of Russian crude oil and petroleum products to global markets, U.S. petroleum net exports rose to 1.4 mb/d, their highest on record since 1947. Consequently, U.S. crude oil inventories remained at their lowest for the month since 2014. Notably, U.S. commercial crude oil inventories between December and April each year on record since 2005 have historically risen by an average of more than 40 million barrels in advance of increased refining activity preceding the summer driving season. As of April 2022 year-to-date, however, U.S. crude oil inventories fell by 3.4 million barrels.

As we have said repeatedly over the past year, a combination of demand outpacing supply, low inventories and import dependence (recently shifted to an increased pull for U.S. energy exports), has historically been a recipe for upward price pressures.

Let us dig into some of the key charts and data from April.

U.S. petroleum demand, as measured by total domestic petroleum deliveries, was 19.3 mb/d in April. This reflected a 5.2% month-on-month (m/m) decrease from March. Excluding the 2020 COVID-19 pandemic, the last time demand fell by more in the month April was in 1989, preceding the 1990-1991 recession.

Furthermore, out of the monthly decrease in demand, more than 90% of it was “other oils” referenced above that feed refinery and petrochemical operations making consumer goods.

Consumer gasoline demand, measured by motor gasoline deliveries, remained near 8.7 mb/d in March and again in April. Excluding the 2020 COVID-19 pandemic, U.S. gasoline demand since 2012 increased by averages of 1.0% m/m between March and April and 3.4% between February and March. Therefore, the past two months departed from and were weaker than these historical monthly changes.

Meanwhile, distillate deliveries of 3.9 mb/d decreased by 2.5% m/m from March and by 3.2% year-on-year (y/y) compared with April 2021. DAT iQ industry trendlines3 showed that spot trucks available in April fell by 2.8% m/m, while the number of available spot loads decreased by 27.0% m/m.

Deliveries of residual fuel oil, which is used as a marine bunker fuel and internationally in electric power production, space heating and industrial applications, were 0.5 mb/d in April, which reflected an increase of 25.6% m/m from March and more than triple (222% y/y) the level in April 2021. Although global marine shipping markets have remained historically tight, it appears likely that fuel substitution of distillates for relatively less expensive residual fuel oil continued in April.

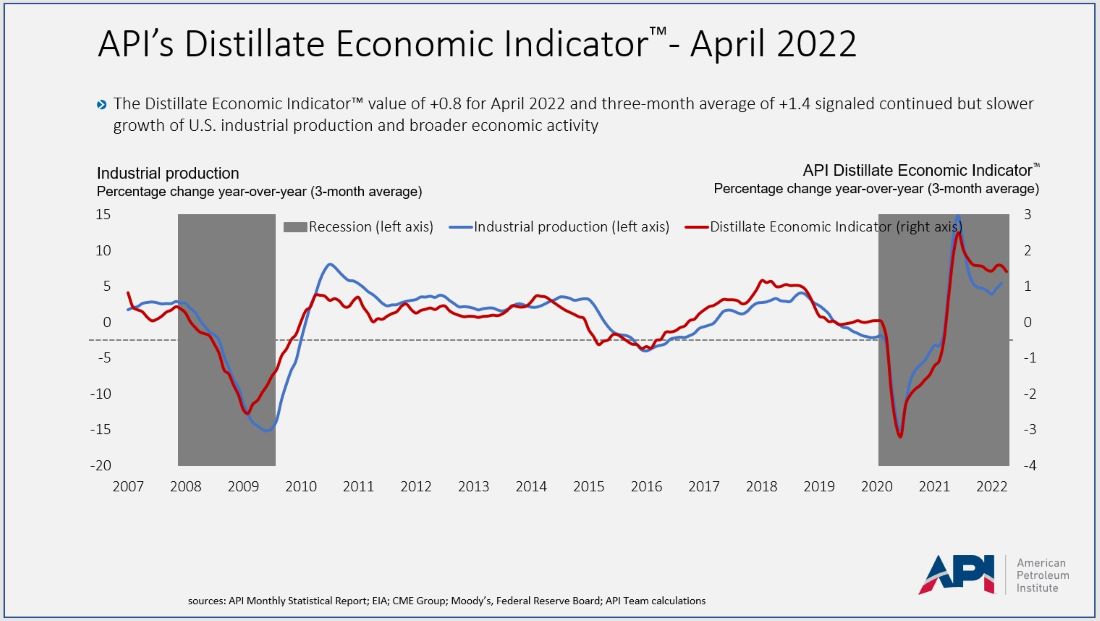

Leading indicators showed weaker industrial growth and consumer sentiment. API’s Distillate Economic Indicator™ suggested slower growth of U.S. industrial production and broader economic activity. However, the University of Michigan’s consumer sentiment index noted broad-based decreases in consumer assessments of current economic conditions as well as expectations.

Although this month’s data appear to offer insight into how consumers have substituted and markets adapted so far this year, the two figures that stood out in April – that is, record-high U.S. petroleum exports and historically low crude oil stock building – should tell policymakers what’s needed to help insulate American households from global volatility. Perhaps now more than ever we need cogent energy policies to spur domestic production, infrastructure construction and trade.

Please see the latest API MSR™ for details, product-level analysis and data.

About The Author

Dr. R. Dean Foreman is API’s chief economist and an expert in the economics and markets for oil, natural gas and power with more than two decades of industry experience including ExxonMobil, Talisman Energy, Sasol, and Saudi Aramco in forecasting & market analysis, corporate strategic planning, and finance/risk management. He is known for knowledge of energy markets, applying advanced analytics to assess risk in these markets, and clearly and effectively communicating with management, policy makers and the media.